When to Say "Yes" to an Offer

You've prepped your home, launched your listing, and now offers are coming in. This should be exciting—but it can quickly become overwhelming.

How do you know if you’re selecting the BEST offer for the home you’re selling?

Believe it or not, it’s not always about the money!

Here are some strategies and tips to keep in mind so that your home is sold to the right buyer, for the right price, and for less stress and anxiety:

1. Know What You Want Most

Before listing your home, decide where you’re flexible and where you’re not.

What matters most?

- Maximum price (even with contingencies/longer timeline)

- Speed (already bought next home, need quick close)

- Certainty (buyer most likely to close)

- Flexibility (need time to move or rent-back)

👉 Tip: Write down your deal breakers ahead of time so you can eliminate weak offers quickly and keep the process moving.

2. Don't Be Swayed by Price Alone

Don’t assume the highest offer is the best offer. Really evaluate each buyer’s entire financial package. There are several factors that can improve a lower offer and guarantee you’ll make it to closing as a happy seller.

Evaluate beyond price:

Down Payment & Financing

Cash = strongest (no contingencies, 2-3 week close, guaranteed)

20%+ down = very strong (conventional financing, less risk)

3-5% down = higher risk (FHA/VA loans add time, appraisal issues common)

Example: $485K FHA offer with 3.5% down vs. $475K conventional with 20% down—many sellers choose the lower offer for certainty and speed.

Earnest Money Deposit

Typical: 1-2% of purchase price

Strong: 3-5% of purchase price

Exceptional: 5%+ of purchase price

A buyer putting $15K-$25K down on a $500K home is unlikely to walk away over minor issues.

Pre-Approval Verification

Request full financial documentation, not just a pre-approval letter. Verify:

- Credit score and debt-to-income ratio

- Employment and income verification

- Down payment source

A lender letter isn't enough. You need the complete financial picture.

Definitely consider buyers who are willing to waive any contingencies or seem willing to work with you on certain terms. No strings attached can be a big plus, even if the price is lower!

3. Understand Contingencies

Every contingency is a condition that could delay or derail closing.

Home Sale Contingency ⚠️ HIGH RISK - Buyer must sell their home first. You're dependent on two transactions.

Inspection Contingency ✓ STANDARD - Normal for buyers to inspect. Watch for reasonable vs. nitpicky negotiators.

Appraisal Contingency ⚠️ MODERATE RISK - If appraisal comes in low, buyer can renegotiate or walk. Strongest buyers offer appraisal gap coverage (e.g., "I'll cover up to $10K if appraisal is low").

Finance Contingency ✓ STANDARD - Buyer must secure financing. Even pre-approved buyers can lose financing if they change jobs, take on debt, or make large purchases before closing.

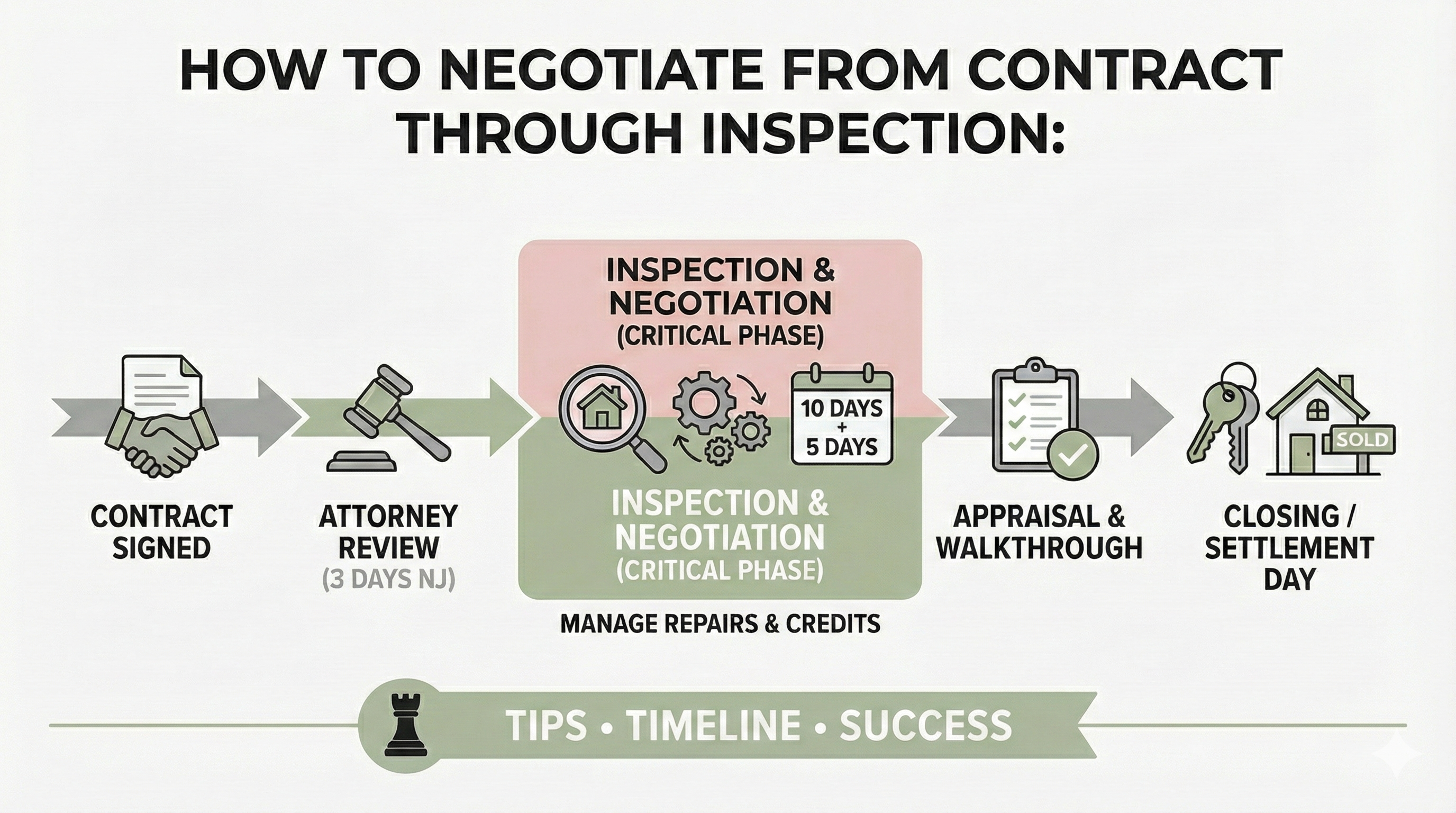

Attorney Review (NJ Standard) - 3-business-day period where either party can modify or cancel. Deals can fall apart here.

4. Timeline & Flexibility Matter

The best offer matches your moving needs.

Need speed? Look for cash buyers (2-3 weeks) or conventional loans with strong pre-approval (30 days).

Need time? Look for buyers offering 45-60 day closings or rent-back arrangements (you stay 30-60 days after closing, typically $50-100/day).

Example: Seller moving to Florida needed 45 days post-closing. Buyer agreed to rent-back at $75/day. This flexibility made a $5,000 lower offer the best choice.

5. Vet Buyer Qualifications Thoroughly

A deal that falls apart after 30-45 days is costly:

- Wasted time

- Increased days on market (red flag to future buyers)

- Lost momentum

- Emotional toll

| Due Diligence Checklist: |

|---|

| ✓ Request full financial documentation |

| ✓ Call lender to verify strength |

| ✓ Check proof of funds for down payment |

| ✓ Verify employment |

| ✓ Review credit score (under 620 is concerning) |

| ✓ Check debt-to-income ratio (under 43% ideal) |

Red flags:

- Won't provide documentation

- Unfamiliar lender with poor reviews

- Down payment from "pending" home sale

- Recent job change

- Low credit score

Your agent should handle this—but insist on seeing information before accepting.

6. Negotiating Offers Strategically

| Evaluate each offer carefully: |

|---|

| ☐ Price - Net proceeds after all costs |

| ☐ Terms - Contingencies, timeline, flexibility |

| ☐ Financing - Type, strength, down payment |

| ☐ Certainty - Likelihood of closing |

Handling Multiple Offers

Options:

1. Accept best offer as-is

2. Counter multiple buyers (If needed, refine the offer so it aligns with your goals.)

3. Request "highest and best" (24-48 hour deadline for final offers)

Respond promptly - Keep momentum, buyers may walk if you stall.

👉 Remember: My role is to represent your interests, filter out risks, and guide you toward the best possible deal.

7. Play Fair in Negotiations

Don’t mislead, stall unnecessarily, and don’t show a lack of appreciation during the negotiation period before you decide on an offer. Disclose the same information to all of the buyers and give them the same deadlines.

Remember, buyers can walk away and not want your home if you seem difficult or you keep changing things. Plus, your overall demeanor could backfire when you’re down to one party and you still need to work with each other to complete the transaction.

It all comes down to “playing nice” while still using strategic negotiation tactics to sell your home.

8. Should You Read Buyer "Love Letters"?

If multiple buyers are vying for your home, each will most likely write a letter and possibly send photos showing that they are the perfect buyers who will love your home just as much as you. Here’s their chance to stand apart from the competition and tug at your emotions as you decide on their offer.

Reading these personal appeals could either make your decision easier or much, much harder. You usually want to make selling your home a straightforward business transaction and not get mixed up in emotions.

However, selling a home you love IS emotional and very personal, so tread lightly here and keep it all in perspective. The more you know about a particular buyer, the harder it may be to disappoint them.

And, these love letters are now getting heat in the real estate industry for not complying with fair housing laws, which is why I always recommend to my sellers not to allow them. If you agree, then I can communicate that to potential buyers and their agents and keep us both safe from fair housing violations.

9. Decision Framework for Choosing the Best Offer

Step 1: Run the Net Numbers

Calculate what you'll actually walk away with after commissions, taxes, fees, attorney costs, mortgage payoff, and any credits.

Example: $500K offer with $5K repair credit vs. $495K with no credits—the $495K offer often nets you more.

Step 2: Check Financing Strength

Cash, loan type, down payment, lender.

| Financing Ranking |

|---|

| Tier 2: Conventional 20%+ down (90-95%) |

| Tier 3: Conventional 10-20% down (85-90%) |

| Tier 4: FHA/VA loans (75-85%) |

| Tier 5: Contingent on selling current home (50-60%) |

Step 3: Evaluate Terms & Contingencies

Fewer contingencies = less risk. Ideal offer has standard inspection only, appraisal gap coverage, substantial earnest money.

Step 4: Match Timeline to Your Needs

Does closing date work? Can they be flexible if needed?

Step 5: Ask: Which Buyer Will Close Smoothly?

Sometimes a slightly lower offer from a stronger buyer is the smartest choice.

The right offer isn't always the highest offer—it's the one that gets you to closing successfully with terms that work for you.

Let's discuss your upcoming sale and create a strategy for attracting strong offers.