Credit Scores Demystified: What Really Impacts Your Credit and How to Fix It

Most of us know our credit score matters — but very few really understand how it's calculated, what hurts it the most, or how to repair it when things go wrong.

Whether you're buying a home, applying for a loan, or simply trying to improve your financial health, your credit score can save you (or cost you) tens of thousands of dollars over time.

In this guide, we'll break down the myths, the facts, and the strategies you need to know to take control of your credit.

Why Negative Items Can Haunt Your Credit for Years

Most negative items (like late payments or collections) stay on your credit report for seven years. If left alone, they eventually fall off on their own.

But here's the catch: if you pay off a collection, it can reset the clock.

Example:

A collection was due to drop off in 2 years. You pay it today. Now it stays for 7 more years from the payment date.

That's why paying off collections may feel like cleanup, but it can actually hurt your credit in the short term.

Medical Collections: What Changed After COVID

Medical debt has always been tricky, but post-COVID reforms brought major changes:

Small balances – Medical collections under $500 no longer appear on credit reports.

Paid collections – Once paid, they must be removed by law.

Underwriting rules – Medical debt is treated differently than credit cards or loans. Lenders know it doesn't reflect borrowing behavior, so it's less of a barrier to getting a mortgage.

Takeaway: If you have medical collections, paying them off now actually helps—they'll be deleted, unlike other types of collections.

The Real Cost of a Low Credit Score

Your score doesn't just affect approval—it affects wealth.

Example on a $500,000 mortgage:

At 5.7% interest:

- Monthly payment: $3,207

- Total interest over 30 years: $604,468

At 7.4% interest:

- Monthly payment: $3,451

- Total interest over 30 years: $740,000+

That's $135,000+ more because of your score.

Why Missing a Payment Is So Expensive

Credit score tiers change interest rates. A higher rate means you pay tens of thousands more over time.

One missed payment can drop your score enough to bump you into a higher rate tier—costing you thousands in additional interest.

Pro tip: Put bills on auto-pay. One mistake can cost you tens of thousands of dollars.

Credit Karma vs. Real Mortgage Scores

Here's what most people don't realize:

Credit Karma shows VantageScore – Mortgage lenders use FICO (industry-specific versions).

It's common for Credit Karma to show 40-60 points higher than what mortgage lenders actually pull.

There are hundreds of scoring algorithms – Each industry (mortgage, auto, credit card) weighs data differently.

Use Credit Karma to monitor trends and errors—not to predict a lender's decision. For mortgage accuracy, check all three bureaus (Experian, Equifax, TransUnion) and review the full reports.

Credit Utilization: The 30% Rule (and the Real Target of 6%)

30% of your score comes from "Amounts Owed"—also called utilization.

The common advice is to keep each card's reported balance under 30% of its limit. But for best results, aim for 6% or less.

How Utilization Works

Scoring models don't see your bank account—they see ratios.

A $500 card maxed out can hurt just as much (proportionally) as a $10,000 card maxed out.

Balances are reported on your statement closing date, not your due date.

Example: If your statement closes on the 4th, pay down your balance by the 3rd for the best results.

The Snowball Strategy for Quick Score Improvement

Pay the smallest balances to 6% or less first for a quick score lift, then roll those payments to the next card.

This strategy works because each card's utilization is scored individually—so getting multiple cards under 6% has a compounding positive effect.

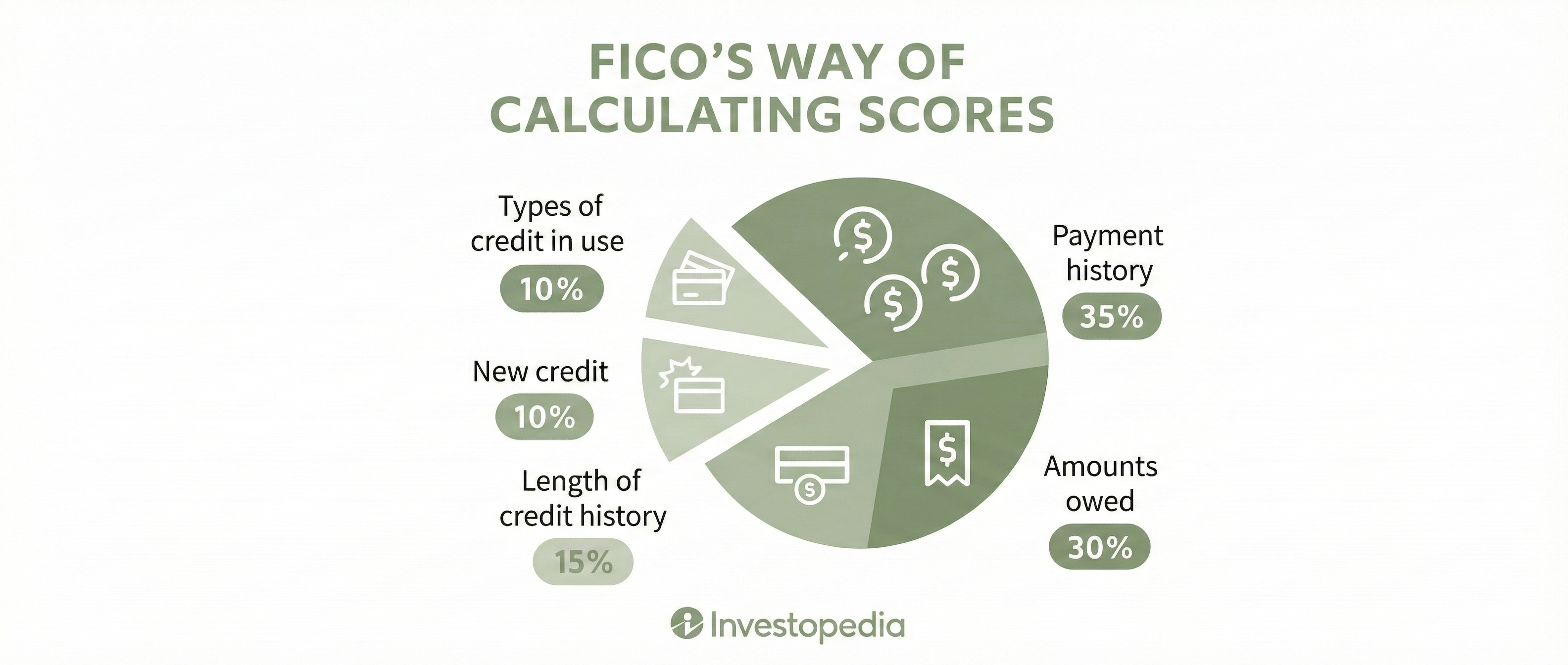

Understanding How Your Credit Score is Calculated

Before we dive into strategies, let's break down what actually impacts your FICO score:

Payment history (35%) – Your track record of on-time payments. This is the single biggest factor.

Amounts owed (30%) – Your credit utilization ratio. How much you owe compared to your credit limits.

Length of credit history (15%) – How long your accounts have been open. Older is better.

New credit (10%) – Recent credit inquiries and newly opened accounts.

Types of credit in use (10%) – Your credit mix: cards, mortgages, auto loans, student loans, etc.

Types of Credit That Matter

Your score values a mix of credit:

- Credit cards (revolving credit)

- Mortgages

- Student loans

- Auto loans

- Personal loans

Important note: A $500 card balance can impact your score more than a $500,000 mortgage. Utilization on revolving credit (cards) weighs heavily, while installment loans (mortgages, auto) have less impact on the "amounts owed" factor.

Credit Mix & Aging: Keep Old Cards Alive

Length of credit history (15% of your score) and credit mix (10%) still matter.

Don't close your oldest card—put a small recurring bill (Netflix, gym membership) on it to keep it active.

You don't need many cards; you need well-managed cards.

If you have no credit cards, open one starter card, use $20-$50/month, and pay it off. Debit cards don't build credit.

What Doesn't Affect Your Credit Score

Contrary to popular belief, these don't impact your score:

- Your income or savings

- How much you've spent on renovations

- Your personal sense of responsibility

- Your job title or employment status

It's based on cold, hard algorithms—and knowing them gives you power.

Bankruptcy and Credit Counseling Programs

Bankruptcies can sometimes be removed from your report, but lender wait periods still apply (typically 2-4 years for conventional mortgages).

Credit counseling often worsens scores—specifically if they require you to stop paying cards. This creates late payments and collections, which tank your score.

Better options:

- Debt restructuring

- Balance transfers to lower-interest credit cards

- Consolidation loans

- Professional credit repair services

If you're considering credit counseling, understand the full impact on your score before enrolling.

The Bottom Line: Credit is Math Plus Timing

Now that you understand the FICO breakdown, focus on the big levers:

35% of your score: Payment history – Never miss a payment. Set up auto-pay. This is your biggest opportunity.

30% of your score: Utilization – Keep reported balances at 6% or less at statement closing. This is your second-biggest lever.

15% of your score: Length of credit history – Keep old cards open and active.

10% of your score: New credit – Limit hard inquiries and space out new accounts.

10% of your score: Credit mix – Having different types of credit helps, but don't open accounts just for mix.

Other key strategies:

Fix errors – Review your credit reports annually and dispute inaccuracies.

Handle medical debt correctly – Pay it to get it removed (unlike other collections).

Avoid moves that re-age old negatives – Don't pay old collections unless they're blocking a loan.

Credit isn't just a number. It's leverage, access, and a wealth-building tool. The difference between a 620 and a 780 score could mean hundreds of thousands of dollars over your lifetime.

With the right knowledge and habits, you can take control—and keep more money in your pocket where it belongs.

If you're working to improve your credit for a home purchase in New Jersey, understanding these fundamentals can save you tens of thousands in interest. The difference between good credit and great credit isn't just approval—it's wealth preservation.